As an entrepreneur, you would like to do business without worries. Timely payment by your (potential) buyers and customers is essential for this. But what if your customers do not honour payment agreements or do not pay at all? How do you find out if a prospect is good for their money? And what about manufacturing and contract risks, foreign exchange problems and political instability? The advice for all these issues is: taking out credit insurance is the wise choice. It will eliminate risks and allow you to actually do business without worries. Below we tell you how credit insurance works, what the benefits are and how Xolv can help you.

In a nutshell: with credit insurance, you still get your money if your customer can no longer pay outstanding invoices. For example, because of liquidity problems, bankruptcy or suspension of payments. You protect your company against non-payment. This prevents your own payment problems or continuity problems. Besides payment of unpaid invoices, credit information and debt collection are also part of the package, which makes taking out credit insurance more than worthwhile.

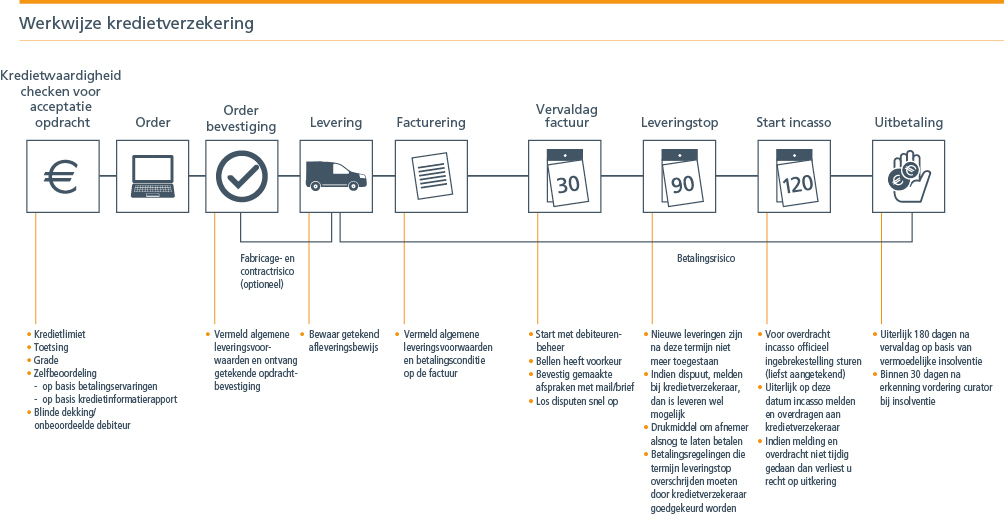

A credit insurance application starts with understanding your customer's financial position. Every credit insurer, including the ones Xolv works with, has a database with up-to-date financial data of companies all over the world. This allows you to check online the creditworthiness check of your (target) buyers and debtors. This is done by analysing hundreds of economic, political, commercial and financial indicators.

Once the insurer has a clear picture of your customer's financial position, they will set a credit limit based on your needs before the delivery begins. This is the amount for which the credit insurer considers it justified to deliver on account to the customer in question. In addition, this is the amount for which you are covered if this customer fails to pay its invoices.

Then you can start doing business. In doing so, it is important that you always state the general terms of delivery and payment terms and put all agreements in writing. While you do business, the credit insurer covers the risks by continuously monitoring your customer's financial position. If necessary, they will adjust the limit in consultation with you during the process.

Whatever measures you take, it can always happen that your customer cannot or will not pay after a delivery. Not even when you send a payment reminder and a reminder. If that is the case, we will find out the reason for non-payment for you. Usually, an amicable solution is preferred, in which we can of course help you. A first step may be to stop supplying products or services, even if there is an obligation to supply on your part.

If the above actions do not help, then collection measures often necessary. The advantage of credit insurers is that they have their own collection agencies worldwide. This allows them - wherever and whenever - to put pressure on your buyers to make payment. Another big advantage is that credit insurers provide cover for multiple suppliers on the relevant buyer, which they reduce or withdraw upon collection. This puts additional pressure on the buyer to pay quickly.

If it turns out that your buyer really cannot pay or even goes bankrupt, the insurer will pay out the insured amount.

This ensures the continuity of your business.

Taking out credit insurance has many advantages. We list the most important ones for you:

With whole-turnover credit insurance, you cover the entire turnover of your business. This means that all your customers and deliveries are insured against the risk of non-payment. By spreading all risks, your cash flow remains stable and you are protected against non-payments across your entire customer base. Ideal for businesses with a broad customer base who want certainty on their revenues.

Sometimes it can be more efficient to insure only specific customers or customer groups. With selective cover, you choose to cover only those customers with higher risk. This provides targeted protection for key risks and can save costs compared to full turnover cover.

Project-based credit insurance allows you to protect payments within a specific project. Useful for sectors such as construction and engineering, where payments are tied to project deadlines. This way, you can be sure of payment even if your customer unexpectedly cannot meet agreements.

If your business is heavily dependent on one customer, single risk insurance offers a solution. This cover focuses specifically on the risk of default by a single key customer. This allows you to do business with confidence and remains protected if this customer defaults.

Do you deal with large purchase orders or payments to international suppliers? Prepayment credit insurance protects you against the risk of a supplier not delivering after payment. This prevents losses if your supplier is unable to meet its obligations, for example due to bankruptcy.

In customised or long-term production runs, there may be a risk that the customer will not pay in the end. Credit insurance at manufacturing and contract level protects your investments during production. Thus, you are assured of payment even if the customer cannot pay on time or at all.

Sometimes exceptional losses arise beyond the usual risk. "Excess of loss" cover provides a cushion against extreme losses above an annual deductible. This cover is a valuable addition for companies looking to protect themselves against unexpected or severe financial hits.

Doing business in international markets involves political risks. Political risk insurance protects you against events such as war, national unrest or government measures that could affect your deliveries or payments. With this cover, you remain assured of stable cash flow even in uncertain geopolitical situations.

Would you like more information on any of these forms of credit insurance or advice on which type of credit insurance best suits your situation? Then take contact with us.

Many think the cost of credit insurance is too high. However, credit insurance costs only a fraction of your turnover. Typically, the cost is between 0.1 and 0.5 per cent of your turnover. The exact cost depends on your turnover, any previous losses, the number of debtors you have (spread of risk) and your debtors' countries of establishment. Moreover, the cost of credit insurance often does not outweigh the losses that can be incurred if you do not have credit insurance.

People think there is a lot of administrative burden attached to credit insurance. That is not correct. Of course, you have to perform a number of actions, but these actually contribute to improving your debtor management and to reducing your debtor risks. Practice shows that in almost all organisations, credit insurance fits perfectly within the existing debtor monitoring. In fact, it often proves to be of absolute added value.

In the Netherlands, more than 80 per cent of all requested limits are issued by credit insurers. These are limits on outstanding to moderately performing companies. Really poorly performing companies or companies that do not want to provide information cannot be insured. It is the role of the credit insurer to check how creditworthy a buyer is. Both the credit insurer and Xolv will pull out all the stops for you to set a limit on your buyer. However, when a credit insurer decides not to cover a buyer, it is wise to ask yourself: should I really want to do business with this non-creditworthy buyer?

This is a very outdated idea. Based on good disclosure, credit insurers can often still maintain cover on struggling companies. One of the most striking examples in recent years is the situation surrounding Vroom & Dreesmann (V&D). Days before V&D went bankrupt, credit insurers were still providing cover based on collateral and good ongoing disclosure. After the bankruptcy, the credit insurer immediately paid out the loss and was then able to recover the full amount from shareholders. Not providing financial data to credit insurers when things are going badly may seem logical but it certainly is not. It is precisely by not providing data that credit insurers are more likely to reduce or withdraw limits.

The right credit insurer helps protect your business against default, optimises your risk management and provides valuable financial insights. That is why we support you in finding the right partner, so that you can be assured that you can run your business carefree.

Want to know more?

Direct quotation request?

Directly transfer intermediation?

Concise product summary (PDF)?

Xolv BV is part of of the Ecclesia Group